— a private valuation prepared for capital partners —

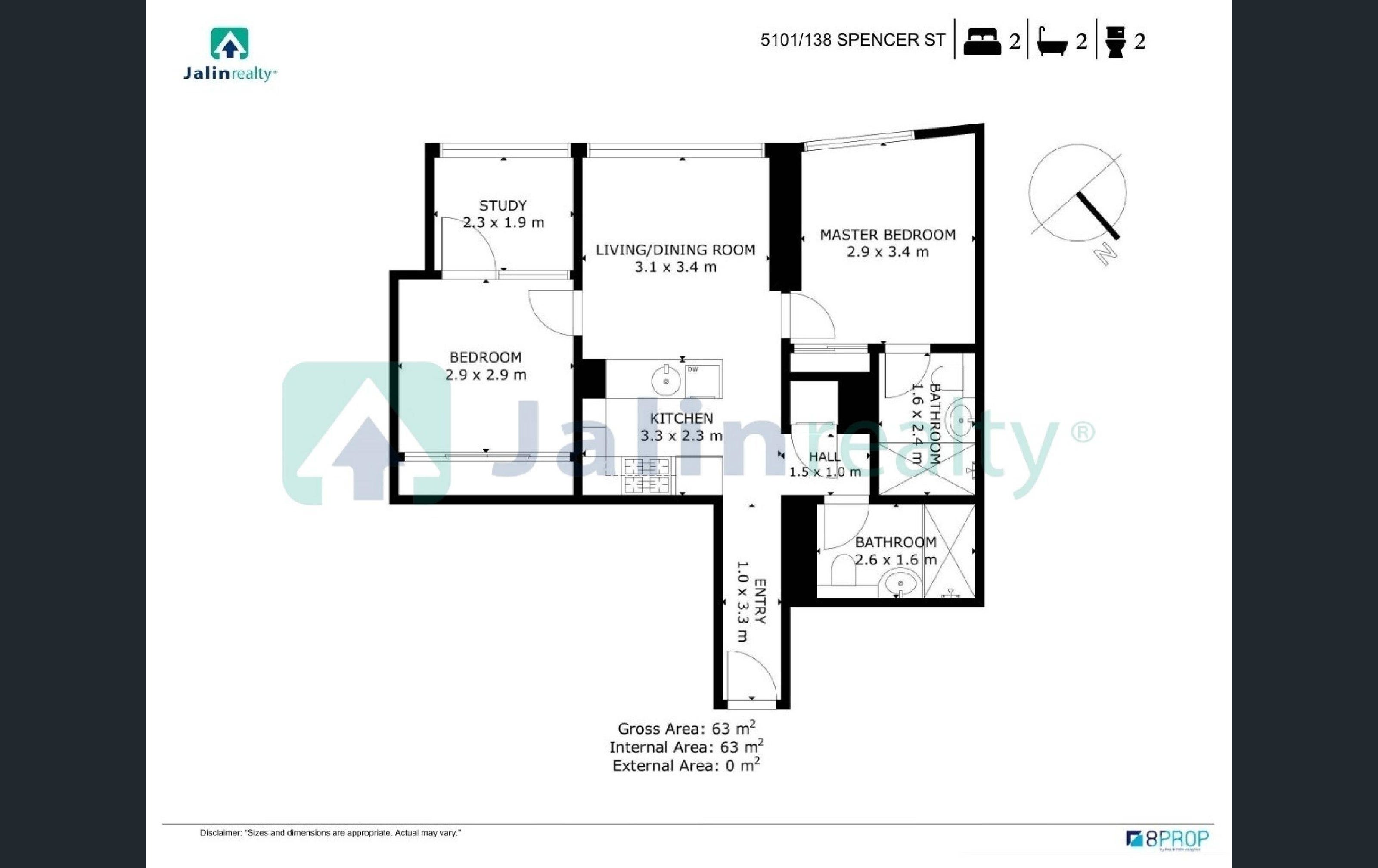

LVL 51·2 BED·2 BATH·0 CAR·63 m²

EXHAUSTIVE

— the upper register · twelve months —

Every recorded sale in the luxury tier (level 39 and above) of Premier Tower between May 2025 and May 2026 from publicly available registers. Forty-seven disposals catalogued. The lower thirty-eight floors are excluded — structurally distinct sub-market, materially higher turnover, lower per-floor pricing — their inclusion in any comparable-sales model would distort the result.

— I —

Position

Premier Tower rises seventy-six storeys above Spencer Street in Melbourne's western central business district. The architectural and pricing midpoint sits at level 38. Everything from level 39 upward forms the upper register — fewer trades, longer holds, materially higher per-floor pricing. Unit 5101 sits at level 51, thirteen floors above midpoint, in the mid-band of this register.

The most apples-to-apples comparators are presumed same-stack units on the "01" line — Unit 5101's exact column. Two such sales settled in the twelve-month window: 7101 (level 71) at $1,069,700 and 3801 (level 38) at $886,800 with a car space. These bracket the subject and anchor the primary estimate. Floorplan equivalence across the "01" line is inferred from unit numbering and is unverified at the cadastral level — see Section VI.

Building Height

76

storeys

Upper Register

L39+

subject sits at L51

Sales Catalogued

47

12 months, top half

Presumed Stack

2

"01" line, inferred

— II —

Visual Reconnaissance

Eighteen interior & outlook photographs, plus a full interactive 360° walkthrough of the unit. The tour is best experienced full-screen — drag to rotate, scroll to move through the floorplan.

All Premier Tower disposals at level 39 and above between 13 May 2025 and 27 May 2026, as reported in the primary public sales register. The adjusted column re-prices each comparable to the subject's configuration (level 51, no car, 63 m²) at current market — applying car-space hedonic (−$75,000), level differential (+/− $2,500 per floor general; +/− $7,815 per floor for the "01" line corner stack, derived in-tower), and a time decay of −3.5% per annum based on observed in-building capital growth.

Unit

Settled

Level

Bd/Ba/Pk

Sale Price

Adjusted to U5101

Note

7101 ◆

13 May 2025

71

2/2/—

$1,069,700

$873,300

"01" line — primary anchor

3801 ◆

09 Jun 2025

38

2/2/1

$886,800

$815,600

"01" line — primary anchor

7207

22 Jan 2026

72

2/2/1

$1,033,300

$896,700

2BR/2BA most recent

7307

19 Aug 2025

73

2/2/1

$1,038,300

$882,900

2BR/2BA with car

7507

26 Jun 2025

75

2/2/—

$1,061,300

$967,300

upper 2BR — 07 corner

7406

08 Jul 2025

74

2/2/—

$1,040,200

$952,200

upper 2BR — 06 corner

6303

09 Oct 2025

63

2/2/0

$959,400

$909,000

2BR/2BA

6309

28 May 2025

63

2/2/—

$946,400

$883,400

2BR — 09 line

6207

08 Oct 2025

62

2/2/—

$898,600

$851,900

2BR/2BA

6107

19 Sep 2025

61

2/2/0

$893,600

$846,900

2BR/2BA

7602

10 Oct 2025

76

2/2/—

$815,300

$736,200

top-floor compact 2BR

6007

09 Oct 2025

60

2/2/0

$888,600

$847,000

2BR/2BA

6006

01 Sep 2025

60

2/2/0

$876,900

$832,900

2BR/2BA

6206

09 Sep 2025

62

2/2/0

$882,700

$833,800

2BR/2BA

6211

02 Sep 2025

62

2/2/—

$822,000

$774,600

2BR — 11 line compact

6306

18 Aug 2025

63

2/2/—

$887,700

$833,700

2BR — 06 corner

6106

30 Jul 2025

61

2/2/—

$881,900

$830,300

2BR — 06 corner

5906

19 May 2025

59

2/2/—

$876,100

$825,300

2BR — 06 corner

5805

20 Aug 2025

58

2/2/0

$872,940

$831,500

2BR/2BA

5503

19 Aug 2025

55

2/1/0

$877,500

$862,700

2BR/1BA — closest level

7503

14 Aug 2025

75

2/—/—

$666,700

$589,700

compact 2BR — different floorplan

7504

30 Sep 2025

75

2/—/—

$671,300

$596,000

compact 2BR — different floorplan

7502

29 Jul 2025

75

2/—/—

$713,800

$633,500

compact 2BR — different floorplan

7208

10 Jul 2025

72

2/—/—

$704,000

$631,300

compact 2BR — different floorplan

4311

02 Jun 2025

43

2/2/0

$690,000

$685,900

low outlier

7505

21 Oct 2025

75

1/1/0

$692,800

—

1BR · context only

7405

16 Oct 2025

74

1/1/0

$691,800

—

1BR · context only

7105

12 Nov 2025

71

1/1/0

$688,800

—

1BR · context only

6905

11 Nov 2025

69

1/1/0

$686,800

—

1BR · context only

6104

27 Nov 2025

61

1/1/1

$733,600

—

1BR with car · context

6204

21 Oct 2025

62

1/1/0

$649,200

—

1BR · context

7305

17 Sep 2025

73

1/—/—

$690,800

—

1BR · context

7404

10 Sep 2025

74

1/—/—

$670,300

—

1BR · context

7304

12 Aug 2025

73

1/—/—

$660,300

—

1BR · context

4202

04 Sep 2025

42

1/1/1

$704,800

—

1BR with car · context

7409

23 Jun 2025

74

1/1/0

$655,600

—

1BR · context

7205

16 Jun 2025

72

1/1/0

$689,800

—

1BR · context

7408

14 May 2025

74

1/—/—

$704,800

—

1BR · context

7203

13 May 2025

72

1/2/0

$664,000

—

1BR · context

3903

10 Dec 2025

39

1/1/0

$530,000

—

1BR · low-floor of register

6710

18 Sep 2025

67

1/1/0

$550,000

—

1BR · weak sale

7605

02 Oct 2025

76

1/—/—

$693,800

—

1BR · context

6404

26 May 2025

64

1/1/0

$658,617

—

1BR · context

7609

28 May 2025

76

1/1/1

$768,000

—

1BR with car · context

7407

25 Jun 2025

74

3/—/—

$940,800

—

3BR · segment differs

7607

13 Jun 2025

76

3/—/—

$1,091,300

—

3BR · segment differs

5101

— Subject —

51

2/2/0

to be set

this dossier

"01" line, level 51, 63 m²

— IV —

Method · Four Cross-Checks

Four independent angles. None is sufficient alone. Treated as cross-checks rather than convergent estimators — they all draw from the same underlying register and are therefore correlated. The role of multiple methods is to surface dispersion, not to validate a point estimate.

— Approach A · "01" Line direct anchor —

Same stack — presumed same floorplan

n=2 · small-sample caveat applies

Per-floor coefficient from 7101 vs 3801 spread (33 floors): $7,815 / floor Caveat: derived from n=2; standard error is large.

From 7101 (L71): $1,069,700 − 20×$7,815 = $913,400; ×0.965 time = $881,000 From 3801 (L38): $811,800 + 13×$7,815 = $913,400; ×0.968 time = $884,000 "01" line mean: $882,500

Approach B · Broad 2BR/2BA sample · adjusted

17 direct matches · level & time adjusted

Mean of 17 adjusted: $860,177 Median: $846,900 Trimmed mean (excl. high & low): $854,300

Approach C · Price per square metre

cross-check via $/m² · industry-standard normaliser

Inferred sqm of comps (Premier Tower standard floorplates): — "01" line corner 2BR: ~70 m² — "06/07" line corner 2BR: ~63-65 m² — "02/03/04/11" compact 2BR: ~55-58 m² Implied $/m² for upper register 2BR/2BA: $13,200 – $14,800 At midpoint $13,800/m² × 63 m² = $869,400 At lower bound $13,200/m² × 63 m² = $831,600 At upper bound $14,400/m² × 63 m² = $907,200 Caveat: sqm of comps inferred, not measured — see Section VI.

Approach D · Settlement-slippage adjustment

advertised prices typically 2 – 5% above settled in soft market

Public-register median of adjusted set: $854,300 Apply −3.5% settlement slippage haircut: ×0.965 ───────────────────────── = $824,400

Range of central estimates

honest dispersion — not a single point

A · "01" line: $882,500 B · broad sample median: $846,900 C · price-per-sqm midpoint: $869,400 D · settlement-adjusted: $824,400 ───────────────────────── Simple mean of four: $855,800 Implied range (min to max): $824,400 – $882,500

— Fair Value · Unit 5101 —

$855,000

— band of confidence · $820,000 to $890,000 —

Walk-Away Floor

$815,000

Target Sale

$855,000

Ambitious Ask

$895,000

— Bear · Contagion —

$795,000

Bottom-half freefall spreads up. Sub-tier sold $635K April 2026 vs $660K February 2026 = annualised −22%. If 30% of that contagion reaches the upper register over 90 days.

— Base —

$855,000

Four-method central estimate. Assumes current upper-register pricing holds with −3.5% p.a. ambient decay through campaign window.

— Bull · Tight Stack —

$895,000

Buyer specifically targets the "01" line corner. Premium paid for north-east aspect and exact floorplan match. Anchors to the higher 7101 print rather than the broad sample.

— V —

Disposition · Economics

At the base-case clearing price of $855,000, transaction costs absorb approximately $23,000 — selling commission 2.0%, marketing $4,000, conveyancing $1,800. Net cash proceeds approximate $832,000. The subject is held against a $473,000 senior mortgage; equity released on close approximates $359,000.

Gross Proceeds

$855,000

base case

Net to Vendor

$832,000

after costs

Equity Released

$359,000

after mortgage payoff

Versus the original acquisition price of $851,000, the base case clears effectively at par. Bear case ($795,000) yields equity release of approximately $300,000. Bull case ($895,000) yields approximately $399,000. The capital-at-risk gradient between bear and bull is therefore $100,000 — the principal range of negotiation leverage.

— VI —

Limitations · Adversarial Review

This dossier rests on a public-register dataset. It is materially less reliable than a sworn certified-practising-valuer report. Below is a candid inventory of structural weaknesses — investors should weigh these before treating any figure above as authoritative.

— Statistical fragility —

The $7,815 per-floor coefficient driving Approach A is derived from two data points. The standard error on that slope is large and unquantified. If either anchor was a motivated or distressed sale, the "01" line analysis collapses to n=1 and the central estimate could move materially in either direction.

— Unverified floorplan equivalence —

The "01" line same-stack assumption is inferred from unit numbering, not from cadastral plans. Premier Tower may have mirror or layout variations across the 33-floor span between the two anchors. Verifying this requires access to the building's title plan or developer floorplate documentation.

— Area inference not measurement —

Square-metre figures for comparables are inferred from Premier Tower standard floorplate conventions, not measured per unit. A single 5 m² mis-estimate at ~$13,800/m² shifts the implied value by approximately $70,000. This is the largest unaddressed variable in the model.

— Advertised vs settled —

Public-register prints are last-known advertised figures, not settlement-confirmed. Soft markets typically print 2–5% above settlement. Approach D captures this generically; instrument-grade settlement data would refine it.

— Bottom-half freefall signal —

Lower-register prints show an annualised pace of decline of approximately −22% over the most recent two-month window (April 2026 sale below February 2026 sale despite higher floor). If this contagion crosses the midpoint, the entire upper-register estimate moves down by 6 – 10% over the next 90 days. The bear scenario assumes 30% contagion transmission.

— Survivorship —

The register shows what sold. It does not show what was withdrawn, passed in at auction, or relisted at lower prices. The current building "for sale" register shows ten listings — modest supply overhang exists. The market may be thinner than closed-sale velocity implies.

— Subject-specific factors not captured —

Aspect, view orientation, finish, furnishing, current owners-corporation fees, days-on-market for the subject itself, and any building-defect status (cladding rectification, structural matters) are not modelled. Each can move the achieved price by ±$30,000.

— Recommended verification —

Cross-validate against settlement-grade paid data sources. Commission a sworn certified-practising-valuer report (approximate cost A$500) before the Statement of Information is finalised under the Estate Agents Act 1980 (Vic). Treat figures above as a structured opening posture rather than as a binding valuation.